Why Acquisition Reform, Contract Consolidation, and AI Mandates Will Reshape How Contractors Compete

Federal contracting has always required resilience, but few years have tested the government contracting (GovCon) market the way 2025 did.

DOGE-led contract reviews, abrupt terminations, and a government shutdown that delayed awards and constrained contracting officer availability forced many contractors into unfamiliar territory. Programs paused and scopes narrowed. Pipelines stalled. In some cases, carefully built forecasts unraveled in a matter of weeks.

While disruptive, these events were also instructive. They surfaced the limits of traditional approaches and accelerated changes that had been gradually reshaping how government contracting organizations operate.

In doing so, 2025 became less a year of disruption and more a catalyst for modernization across the market.

When Stress Tests Expose the Limits of Traditional GovCon Models

The combined effects of DOGE contract reviews and the shutdown placed unprecedented scrutiny on contract value, performance outcomes, and cost justification.

Several vulnerabilities surfaced across the market:

- Lengthy acquisition timelines that limited agencies’ ability to respond quickly to modern mission needs

- Complex contracting pathways that added time and administrative burden to awards and modifications

- Limited flexibility during funding disruptions, particularly when schedules or scopes needed to adjust

In response, many contractors began tightening delivery models, sharpening performance metrics, and reassessing how they aligned resources to agency priorities. More importantly, 2025 made something unmistakable: federal policy direction was no longer incremental. The shift toward speed, efficiency, and commercial alignment was underway.

Executive Actions in 2025 Set the Conditions for 2026

While market volatility captured headlines, a quieter and more consequential shift was happening through executive action.

Executive orders issued throughout 2025 signaled a clear move away from legacy acquisition approaches and toward a more streamlined, commercially aligned procurement environment.

The Ensuring Commercial, Cost-Effective Solutions executive order reinforced the expectation that agencies prioritize commercially available technologies wherever practicable. Modernizing Defense Acquisitions emphasized speed to capability, elevating flexibility and alternative pathways over rigid process adherence.

In parallel, executive actions focused on AI policy removed barriers to adoption and established a whole-of-government framework for integration. Combined with ongoing FAR streamlining efforts, these actions did more than signal reform. They removed long-standing constraints on how agencies could buy.

The executive actions of 2025 were about enabling agencies to move faster, with fewer constraints.

2026: Where Policy Direction Becomes Market Reality

What distinguishes 2026 is not the introduction of new reforms, but their execution.

While adoption is uneven, agencies are beginning to experiment with the flexibility enabled by recent policy changes. In some procurements, this is translating into more outcome-focused solicitations and greater discretion in how contracting officers structure awards.

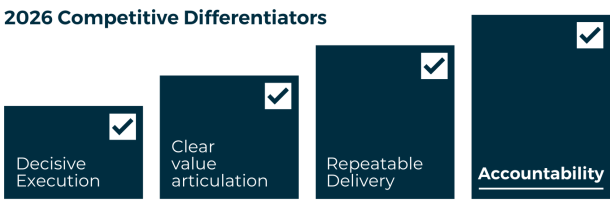

For contractors, this fundamentally reshapes the basis of competition. Success will increasingly depend on the ability to move decisively, articulate value succinctly, and deliver without unnecessary complexity.

While many solicitations remain compliance-heavy, organizations built around long proposal cycles and rigid approval structures may face growing pressure to adapt as acquisition approaches evolve. Those structured for speed, clarity, and accountability will gain ground.

Contract Consolidation Is Narrowing the Competitive Field

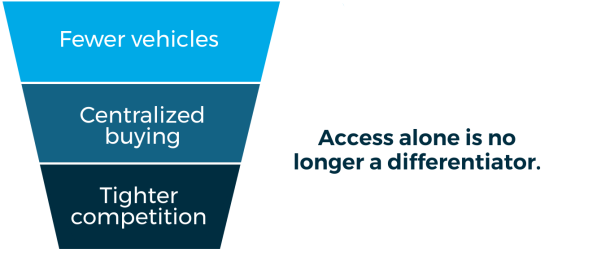

At the same time acquisition pathways are simplifying, the government contracting market itself is consolidating.

Agencies are leaning more heavily on existing contract vehicles, category management strategies, and centralized buying frameworks. The result is fewer entry points and more intense competition within established channels.

This changes how opportunity should be evaluated. Access alone is no longer a differentiator. Contractors must also be easy to engage, responsive at the task level, and aligned with how agencies prefer to buy and manage work.

In a consolidated market, operational fit matters as much as technical qualification.

AI Adoption Shifts from Strategy to Operational Leverage

AI is no longer framed as a future capability in federal contracting. It is increasingly treated as an operational expectation.

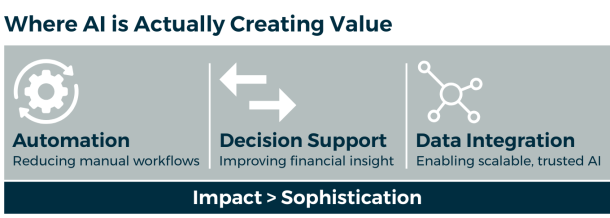

As agencies work to offset workforce constraints and administrative burden, demand is accelerating in several specific areas.

- Process automation and orchestration to reduce manual workflows in finance, procurement, compliance, and reporting

- Decision support and analytics tied directly to mission, financial integrity, and operational oversight

- Data integration and quality management to enable AI use at scale while maintaining auditability and trust

The fastest growth is not coming from experimental models or abstract use cases. It is coming from AI applied directly to execution. Solutions that automate repeatable processes, improve consistency, and reduce cycle time are delivering immediate value.

In this environment, sophistication matters less than impact. AI that cannot be operationalized quickly or governed responsibly will struggle to scale.

Governance Defines AI Readiness in Practice

As AI becomes embedded in operational environments, scrutiny increases accordingly.

Agencies are placing greater emphasis on how AI-enabled systems are governed, monitored, and controlled. Questions of data integrity, cybersecurity, risk management, and auditability are now central to acquisition and performance discussions.

Demonstrating capability is no longer sufficient. Contractors must explain how AI outputs are validated, how risk is managed over time, and how systems align with mission outcomes.

The firms best positioned for 2026 will be those that treat governance as a design principle, not a compliance afterthought.

Execution Discipline Becomes the Ultimate Differentiator

Perhaps the most consequential shift heading into 2026 is the increased emphasis on execution discipline.

While solicitation structures and timelines vary widely across agencies, expectations for post-award performance continue to intensify. Programs are operating under greater scrutiny, with increased attention on outcomes, cost justification, and delivery consistency throughout the period of performance.

In this environment, agencies gravitate toward partners that demonstrate repeatable delivery models, clear governance, and the ability to perform reliably under changing conditions.

Innovation may open the door, but execution determines who stays.

What This Means for Contractors Preparing for 2026

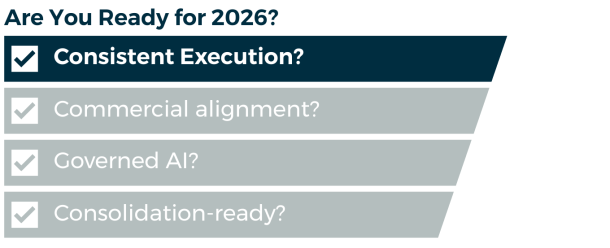

As these forces converge, contractors should assess readiness with intention. The following questions are not theoretical. They are practical indicators of competitiveness in the year ahead:

- Are we structured to deliver more consistently under evolving acquisition expectations?

- Are our offerings aligned with commercial buying expectations?

- Can we clearly articulate how AI is governed within our solutions?

- Are we prepared to compete effectively within a consolidated market?

The value of asking these questions lies in action. Organizations that address gaps now will be better positioned as acquisition behavior continues to evolve.

A Clear Imperative for the Year Ahead

The disruptions of 2025 challenged long-standing assumptions across government contracting. The changes unfolding in 2026 will determine which contractors adapt and which are left behind.

This is no longer a period for observation or commentary. It is a moment that rewards preparation, discipline, and execution.

For contractors willing to evolve how they compete and deliver, 2026 presents meaningful opportunity. For those anchored to legacy models, the market may move on without them.

The advantage will belong to firms that translate reform into results.